Don’t Overestimate China’s Inflationary Impact

Commentary The so-called restart of the Chinese economy has largely just echoed the market. But some suggest this will give a new push to global inflation when strong demand from China drives the resource markets. However, maybe we should revisit the basics: Where does that strong demand for Chinese production come from? Isn’t China the factory for the world? But if the rest of the world has sluggish demand due to inflation and rising interest rates, will this still be the same story as that of a decade ago? For this inflation conjecture to be true, China’s restart should have booted up its own inflation before sending goods to other countries. But as the accompanying chart shows, even the first part of this logic fails. According to the basics of monetary theory (or even common sense), inflation is always a result of too much money or money turnover being too fast. China’s monetary authority, the People’s Bank of China (PBoC), has been accelerating the economic base, but the velocity has remained low, given that year-over-year credit growth is staying stagnant. China loans and CPI YoY growth. Feb. 27, 2023.(Courtesy of Law Ka-chung) The one-off stronger number in January did not change the trend. The accompanying chart shows that the growth trend of loans remains subdued at a two decades’ low. But there is a time lag between credit and inflation. Empirically the time lag for China is about five quarters, as is evident from the chart. Then inflation is still projected on a downtrend for at least another year until Spring 2024. If this comes true, China cannot export inflation to the rest of the world, as is claimed. Central banks worry about the inextinguishable inflation, but what is the source? Examine the breakdown of inflation, and it’s the services sector that generated the recent round of inflation. Indeed the same is true for inflationary pressure in China and Hong Kong. The experience of Japan in the 1990s and the U.S. after 2008 suggest inflation is much more prone to money velocity than its amount. The velocity of money should be low against the backdrop of China’s deleveraging and other countries’ tightening. We do see inflation taming, although at an unsatisfactory pace. What makes it slow? While debt deleveraging in China and rate hikes elsewhere are effective in retarding credit, liquidity is still abundant: nowhere has a very restrictive interest rate level, and nowhere has undergone a persistent contraction of the monetary base so far. However, central banks still worry about overdoing rates and creating a recession. Ironically, however, a recession is often needed to bring down inflation, especially when it is high enough with expectations unanchored. In the past two years, when China faced disinflationary pressure, this did not transmit effectively to the rest of the world. There is no solid reason to suggest China’s inflationary pressure, if any, would spread globally. Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Commentary

The so-called restart of the Chinese economy has largely just echoed the market. But some suggest this will give a new push to global inflation when strong demand from China drives the resource markets. However, maybe we should revisit the basics: Where does that strong demand for Chinese production come from? Isn’t China the factory for the world? But if the rest of the world has sluggish demand due to inflation and rising interest rates, will this still be the same story as that of a decade ago?

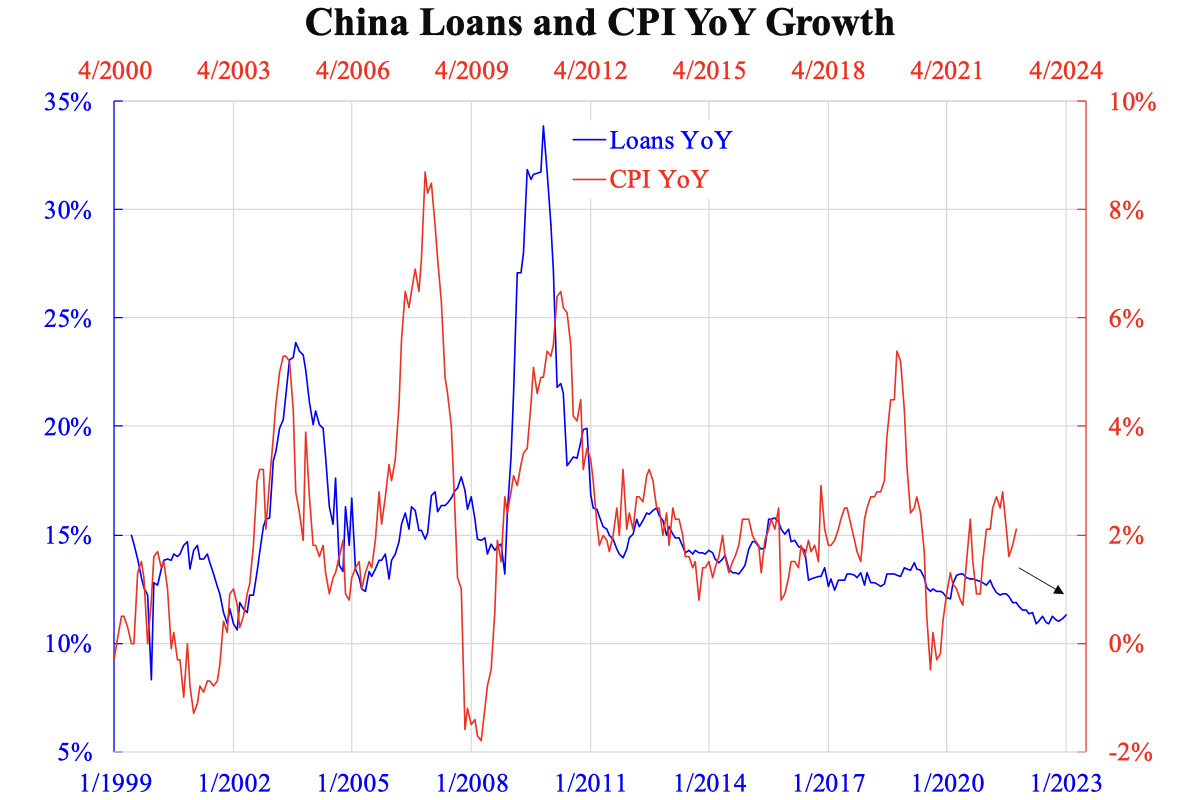

For this inflation conjecture to be true, China’s restart should have booted up its own inflation before sending goods to other countries. But as the accompanying chart shows, even the first part of this logic fails. According to the basics of monetary theory (or even common sense), inflation is always a result of too much money or money turnover being too fast. China’s monetary authority, the People’s Bank of China (PBoC), has been accelerating the economic base, but the velocity has remained low, given that year-over-year credit growth is staying stagnant.

The one-off stronger number in January did not change the trend. The accompanying chart shows that the growth trend of loans remains subdued at a two decades’ low. But there is a time lag between credit and inflation. Empirically the time lag for China is about five quarters, as is evident from the chart. Then inflation is still projected on a downtrend for at least another year until Spring 2024. If this comes true, China cannot export inflation to the rest of the world, as is claimed.

Central banks worry about the inextinguishable inflation, but what is the source? Examine the breakdown of inflation, and it’s the services sector that generated the recent round of inflation. Indeed the same is true for inflationary pressure in China and Hong Kong. The experience of Japan in the 1990s and the U.S. after 2008 suggest inflation is much more prone to money velocity than its amount. The velocity of money should be low against the backdrop of China’s deleveraging and other countries’ tightening.

We do see inflation taming, although at an unsatisfactory pace. What makes it slow? While debt deleveraging in China and rate hikes elsewhere are effective in retarding credit, liquidity is still abundant: nowhere has a very restrictive interest rate level, and nowhere has undergone a persistent contraction of the monetary base so far. However, central banks still worry about overdoing rates and creating a recession. Ironically, however, a recession is often needed to bring down inflation, especially when it is high enough with expectations unanchored.

In the past two years, when China faced disinflationary pressure, this did not transmit effectively to the rest of the world. There is no solid reason to suggest China’s inflationary pressure, if any, would spread globally.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.