CNY Mainly ‘Internationalized’ in Offshore Hong Kong

CommentaryRecently, Xi Jinping of mainland China visited Saudi Arabia, arousing speculation of some new deals to be done. Specifically, some nationalists expect a substantial portion of Saudi oil exported to China to be settled in the Chinese Yuan (CNY) rather than the U.S. dollar. Such wishful thinking is obviously self-defeating by looking at the data: Saudi Arabia has been running a huge trade surplus from China, and they will be accumulating CNY over time without an effective way to channel it back to mainland China. Naturally, that was empty talk. In deciding whether to accept CNY, another practical consideration is its popularity in usage. To see how one currency penetrates into another country, the best is to refer to the triennial survey done by the Bank for International Settlements (BIS). There are other statistics, such as the SWIFT payments system by currency settled, but the whole globe’s transactions are lumped together without breaking down each country. Although BIS’ survey is done only once every three years where the latest being in April 2022, it breaks things down like an input-output table. According to the global result, CNY ranked the fifth largest currency in over-the-counter (OTC) foreign exchange (FX) turnover, taking up 3.5 percent of the total turnover. On the surface, this is even higher than the share in SWIFT payments at around three percent. However, there is a tricky point in such accountings: Since Hong Kong is regarded as offshore of China, any turnover or transactions happening here are not onshore and are regarded as “international payments.” However, as we all know, these are not really anything international but just within the loop. CNY turnover by country, as percent share of all countries; Dec. 14, 2022. (Courtesy of Law Ka-chung) The accompanying chart shows CNY turnover by country; remember, the total here adds up to the just mentioned 3.5 percent of the world share. There are actually 52 reported places, but here we show the first ten (and one more), which are more than sufficient as the shares at the sixth place (Taipei) onward are substantially lower than the fifth. The most striking place is Hong Kong: the highest turnover place taking up 28 percent. Interestingly, the third-ranked turnover is mainland China itself. These two shares already add up to 45 percent, nearly half the total. Excluding these, CNY is effectively being used in the UK, Singapore, and the U.S., of which two of them do not have a good relationship with mainland China. The regionalization of CNY is not promising at all, given its low presence in Asian countries. If, one day, CNY’s usage in the UK and/or the U.S. is limited, the total outstanding of “international CNY” will decline substantially. By then, Singapore remains the truly offshore CNY centre (apart from Hong Kong). Thus, the so-called CNY internationalization is essentially targeting only Singapore. The funniest thing is probably Saudi Arabia, which ranked 40th in trading CNY among 52 countries. They almost don’t use this currency, yet some Chinese nationalists expect them to sell crude oil by receiving CNY. Even Hong Kong people are generally unwilling to receive CNY, a depreciating currency paying too low interest. Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times. Follow Law Ka-chung is a commentator on global macroeconomics and markets. He has been writing numerous newspaper and magazine columns and talking about markets on various TV, radio, and online channels in Hong Kong since 2005. He covers all types of economics and finance topics in the United States, Europe, and Asia, ranging from macroeconomic theories to market outlook for equities, currencies, rates, yields, and commodities. He has been the chief economist and strategist at a Hong Kong branch of the fifth-largest Chinese bank for more than 12 years. He has a Ph.D. in Economics, MSc in Mathematics, and MSc in Astrophysics. Email: [email protected]

Commentary

Recently, Xi Jinping of mainland China visited Saudi Arabia, arousing speculation of some new deals to be done. Specifically, some nationalists expect a substantial portion of Saudi oil exported to China to be settled in the Chinese Yuan (CNY) rather than the U.S. dollar. Such wishful thinking is obviously self-defeating by looking at the data: Saudi Arabia has been running a huge trade surplus from China, and they will be accumulating CNY over time without an effective way to channel it back to mainland China. Naturally, that was empty talk.

In deciding whether to accept CNY, another practical consideration is its popularity in usage. To see how one currency penetrates into another country, the best is to refer to the triennial survey done by the Bank for International Settlements (BIS). There are other statistics, such as the SWIFT payments system by currency settled, but the whole globe’s transactions are lumped together without breaking down each country. Although BIS’ survey is done only once every three years where the latest being in April 2022, it breaks things down like an input-output table.

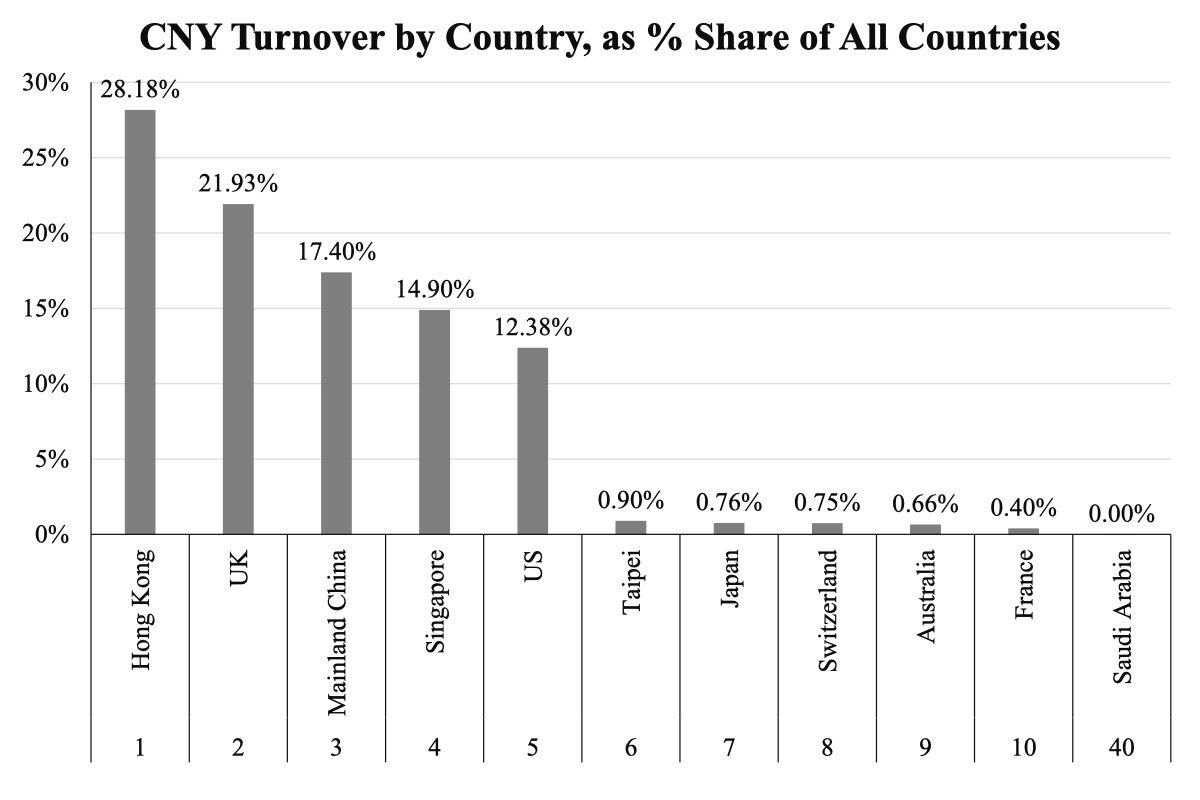

According to the global result, CNY ranked the fifth largest currency in over-the-counter (OTC) foreign exchange (FX) turnover, taking up 3.5 percent of the total turnover. On the surface, this is even higher than the share in SWIFT payments at around three percent. However, there is a tricky point in such accountings: Since Hong Kong is regarded as offshore of China, any turnover or transactions happening here are not onshore and are regarded as “international payments.” However, as we all know, these are not really anything international but just within the loop.

The accompanying chart shows CNY turnover by country; remember, the total here adds up to the just mentioned 3.5 percent of the world share. There are actually 52 reported places, but here we show the first ten (and one more), which are more than sufficient as the shares at the sixth place (Taipei) onward are substantially lower than the fifth. The most striking place is Hong Kong: the highest turnover place taking up 28 percent. Interestingly, the third-ranked turnover is mainland China itself. These two shares already add up to 45 percent, nearly half the total.

Excluding these, CNY is effectively being used in the UK, Singapore, and the U.S., of which two of them do not have a good relationship with mainland China. The regionalization of CNY is not promising at all, given its low presence in Asian countries. If, one day, CNY’s usage in the UK and/or the U.S. is limited, the total outstanding of “international CNY” will decline substantially. By then, Singapore remains the truly offshore CNY centre (apart from Hong Kong). Thus, the so-called CNY internationalization is essentially targeting only Singapore.

The funniest thing is probably Saudi Arabia, which ranked 40th in trading CNY among 52 countries. They almost don’t use this currency, yet some Chinese nationalists expect them to sell crude oil by receiving CNY. Even Hong Kong people are generally unwilling to receive CNY, a depreciating currency paying too low interest.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.