China Is Still What It Used to Be

Commentary The recent China data often shocked the market, foreigners, and local analysts. Sometimes it was a fight between the official and private data sources like PMI; sometimes, it was a mismatch between domestic and foreign sources like trade data. A few years ago, China data were well-known to be fake: Whatever number the government claimed a figure should be, it would turn out to be that number. However, data look less abnormal in recent years than in the olden days. Yet, the official releases are still far from our actual understanding. In the past, when Western countries did plan to open up a more than one billion market in China, they would pay special attention to the domestic economic performance. After a series of events, including the new cold war and lockdowns, Western countries have lost their interest in China. China’s domestic economic performance is no longer in their interests. But they still want to know China’s external economic performance as this reflects the strength of the communist camp. Of course, this would interest the government more than the business level. Data that have the least chance of being fake are the balance of payments (BoP). One country’s out means the others’ in; the grand total must be zero. In this sense, BoP compiled under the unified methodology by the International Monetary Fund (IMF) should be a reliable source, albeit the latest available quarterly data are 2022Q4 instead of 2023Q1 (some emerging countries report with delay). In the accompanying chart, China’s net exports of goods and services, as well as corresponding financial flows, including direct and portfolio investments, are shown. (Courtesy of Law Ka-chung) China is still highly reliant on goods exports to earn foreign exchange. Goods export growth was the strongest in the 2000s but were much weaker in the 2010s after the financial tsunami and European debt crisis. In the first few years of the 2020s, the growth was mid-level. Yet the chart showing a flat level (of the red line) over the past few years means stagnant growth, which agrees with headline export growth data. Services exports were never the focus because China did not open the market, so services could hardly export. Net direct investment is conceptually similar to foreign direct investment (FDI). It surged briefly after the COVID-19 outburst but dipped into a contraction in recent quarters. Worst of all is the net debt investment under portfolio flow, thanks to the series of debt defaults in recent years. Equity investment has never been strong, which is unsurprised, given the sluggish trend of the A-shares market. In a word, China failed to bring in much financial capital, but forex was earned from selling goods (not services). Today it is still a world factory. West countries are honest in that they are not de-Chinalising but are still consuming China. Such a power structure is not fundamentally different from previous decades and is unlikely to change in the decade ahead. Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.

Commentary

The recent China data often shocked the market, foreigners, and local analysts. Sometimes it was a fight between the official and private data sources like PMI; sometimes, it was a mismatch between domestic and foreign sources like trade data.

A few years ago, China data were well-known to be fake: Whatever number the government claimed a figure should be, it would turn out to be that number.

However, data look less abnormal in recent years than in the olden days. Yet, the official releases are still far from our actual understanding.

In the past, when Western countries did plan to open up a more than one billion market in China, they would pay special attention to the domestic economic performance.

After a series of events, including the new cold war and lockdowns, Western countries have lost their interest in China. China’s domestic economic performance is no longer in their interests. But they still want to know China’s external economic performance as this reflects the strength of the communist camp. Of course, this would interest the government more than the business level.

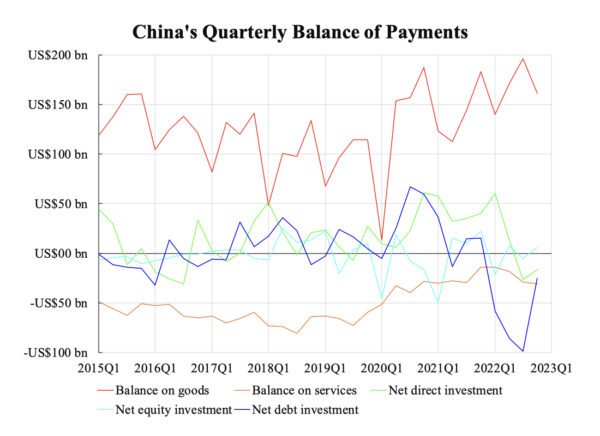

Data that have the least chance of being fake are the balance of payments (BoP). One country’s out means the others’ in; the grand total must be zero. In this sense, BoP compiled under the unified methodology by the International Monetary Fund (IMF) should be a reliable source, albeit the latest available quarterly data are 2022Q4 instead of 2023Q1 (some emerging countries report with delay).

In the accompanying chart, China’s net exports of goods and services, as well as corresponding financial flows, including direct and portfolio investments, are shown.

China is still highly reliant on goods exports to earn foreign exchange. Goods export growth was the strongest in the 2000s but were much weaker in the 2010s after the financial tsunami and European debt crisis. In the first few years of the 2020s, the growth was mid-level. Yet the chart showing a flat level (of the red line) over the past few years means stagnant growth, which agrees with headline export growth data. Services exports were never the focus because China did not open the market, so services could hardly export.

Net direct investment is conceptually similar to foreign direct investment (FDI). It surged briefly after the COVID-19 outburst but dipped into a contraction in recent quarters. Worst of all is the net debt investment under portfolio flow, thanks to the series of debt defaults in recent years.

Equity investment has never been strong, which is unsurprised, given the sluggish trend of the A-shares market. In a word, China failed to bring in much financial capital, but forex was earned from selling goods (not services). Today it is still a world factory.

West countries are honest in that they are not de-Chinalising but are still consuming China. Such a power structure is not fundamentally different from previous decades and is unlikely to change in the decade ahead.

Views expressed in this article are the opinions of the author and do not necessarily reflect the views of The Epoch Times.